Family finances can feel easier to manage when everyone is working toward a clear purpose. Without goals, money often moves in too many directions at once. Bills get paid, purchases happen and savings may be left to whatever remains.

That approach can work for a short time, but it rarely gives a household the structure needed for long-term stability.

Family financial goals help turn income into a plan. They give parents, partners and children a shared understanding of what matters most. Some goals may be small, such as saving for school supplies.

Others may take years, such as buying a home or preparing for retirement. The key is to make each goal clear, realistic and connected to everyday choices.

What Are Family Financial Goals?

Family financial goals are shared money targets that a household works toward together. These goals can cover saving, spending, debt, investing or planning for future needs. They can also include teaching children how money works.

A short-term goal might be building a small emergency fund or paying off one credit card. A medium-term goal could be saving for a home repair, a vehicle or a family trip. A long-term goal may include retirement savings, college costs or paying off a mortgage.

The best goals are specific. “Save more money” is too broad. “Save $2,000 for emergency expenses by the end of the year” gives the family something clear to measure.

Why Family Financial Goals Matter

Goals create direction. When a family knows what it is working toward, it becomes easier to decide where money should go. This does not mean every dollar has to feel restricted. It means spending choices become more intentional.

Goals can also reduce stress. A surprise medical bill, car repair or school expense feels less disruptive when there is money set aside. Planning ahead does not remove every financial problem, but it can make problems easier to handle.

Clear goals also improve communication. Money can be a tense topic in many households. A shared plan helps move the conversation from blame to problem-solving.

For families with loved ones in other countries, even practical questions like how to send money internationally can become part of a larger financial plan when support, fees and timing are discussed in advance.

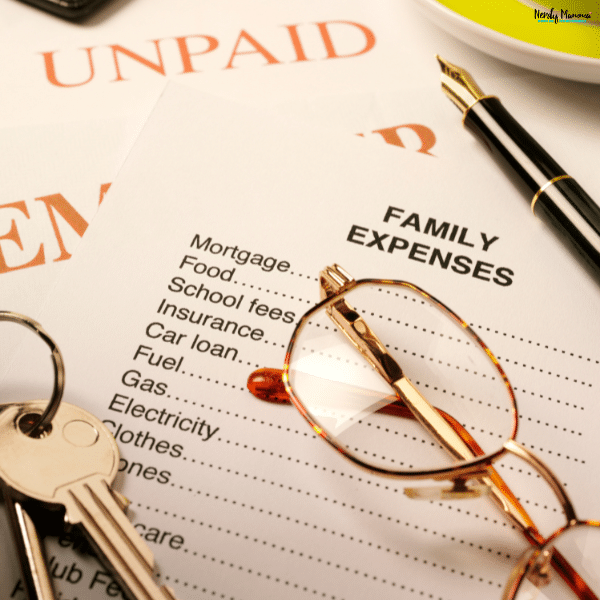

Start With a Clear Picture of Your Current Finances

Before setting goals, review where the household stands today. Start with income. Include wages, self-employment income, benefits, child support, side work or any other steady source of money.

Next, list monthly expenses. Fixed expenses may include rent, mortgage payments, utilities, insurance, childcare and loan payments. Variable expenses may include groceries, fuel, clothing, school costs, entertainment and medical needs.

Then review debt and savings. Write down credit card balances, personal loans, car loans, student loans or medical debt. Also list current savings, emergency funds, retirement accounts and education savings. This step may feel uncomfortable, but it gives the family a real starting point.

Set Short-Term Family Financial Goals

Short-term goals are usually goals that can be reached within one year. These goals help families build momentum because progress can happen quickly.

Examples include saving one month of expenses, starting a holiday fund, paying off a small debt or reducing grocery spending by a set amount. A short-term goal might also be creating a basic household budget and following it for three months.

Keep these goals realistic. If money is tight, start small. Saving $25 each week is still progress. The goal is to build trust in the process. Once the family sees that a plan can work, bigger goals become easier to approach.

Set Medium-Term Family Financial Goals

Medium-term goals often take one to five years. These goals require more planning because they are usually larger than short-term targets.

A family may want to save for a down payment, pay off a car loan, build three to six months of emergency savings or prepare for a major home repair. Other examples include saving for a large family trip, private school costs or a new baby.

The best way to handle medium-term goals is to break them into monthly targets. For example, if a family wants to save $6,000 in two years, it needs to set aside $250 each month. Breaking the number down makes the goal feel more manageable.

Set Long-Term Family Financial Goals

Long-term goals usually take more than five years. They often shape the future of the household. Retirement savings, college planning, mortgage payoff and building wealth all fall into this category.

These goals depend on consistency. Small regular contributions can matter over time. Families should review long-term goals at least once or twice a year to make sure they still fit current income, expenses and life plans.

Long-term goals may not feel urgent when children are young or retirement seems far away. Still, starting early gives a family more options later.

Prioritize Your Family’s Goals

Most families cannot fund every goal at once. That is normal. The first step is separating needs from wants.

Financial stability should usually come first. This includes essential bills, emergency savings, insurance coverage and high-interest debt. Once the basics are steady, the family can add goals such as travel, home upgrades or special events.

Balance matters. A family budget should support the future without making daily life feel joyless. Setting aside money for simple activities or occasional treats can help the plan feel sustainable.

Create a Family Budget Around Your Goals

A budget turns goals into action. It shows how much money comes in, how much goes out and how much can be directed toward specific priorities.

Build goal categories into the budget. These may include emergency savings, debt payments, education costs, home repairs, family activities and retirement contributions. Treat these categories like regular bills when possible.

A budget should not be rigid forever. If income changes or expenses rise, adjust the plan. The goal is not perfection. The goal is steady progress.

Involve the Whole Family

Family financial goals work better when everyone understands the basics. Children do not need to know every detail, but they can learn simple lessons about saving, spending and tradeoffs.

Younger children can use savings jars or help compare prices at the store. Older children can help plan a low-cost activity or learn how a family budget works. These small lessons build useful habits.

Couples should also talk openly about money. A monthly check-in can help both partners review progress, make changes and avoid surprises.

Track Progress and Celebrate Milestones

Tracking keeps goals visible. Review the numbers each month. Look at what was saved, what was spent and what needs to change.

Celebrate progress in simple ways. Paying off one bill, reaching the first $500 in savings or staying on budget for a full month are all worth noting. Small wins help the family stay motivated.

Life will change. A new job, move, medical expense or new child may shift the plan. When that happens, update the goals instead of abandoning them.

Common Mistakes to Avoid

One common mistake is setting too many goals at once. Focus usually works better than trying to fix everything at the same time.

Another mistake is ignoring emergency savings. Without a cushion, one unexpected cost can interrupt every other plan. Families should also avoid guessing where money goes. Tracking spending is one of the simplest ways to find room for improvement.

Finally, do not give up after one setback. A missed savings month does not mean the plan failed. It means the plan needs another look.

Final Thoughts

Family financial goals give a household structure, direction and confidence. They help families prepare for daily needs, unexpected costs and long-term plans.

Start with one short-term goal and one long-term goal. Write them down. Build them into the budget. Review progress often. Over time, small decisions can create real financial strength for the whole family.